On January 7th, 2020, Elon Musk surpassed Jeff Bezos as the richest person in the world. Propelled by Tesla’s seemingly unstoppable rise to an over $770 billion market capitalization, Musk’s net worth swelled to $185 billion. To the surprise of no one, the indictment of the growing wealth of the über rich began immediately. And while this collective indignation may in truth be righteous, it needs to be framed accurately.

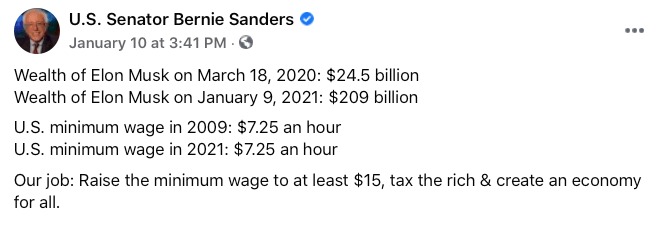

Among those expressing their frustration was Bernie Sanders who showed how within less than a year, Musk had grown his wealth from $24.5 billion to $209 billion—a truly staggering increase. He then compared that increase to the stagnant US minimum wage. Now whatever your thoughts on the minimum wage and its usefulness as an indicator of income inequality, we can take the core message here: in this economy the rich get richer while everyone else faces wage stagnation and limited upward mobility. We could point to a few examples of this being the case. We could show that real wages have stayed mostly the same for decades and that the income gap is indeed widening, but I want to focus on the problem with the way these issues are being presented in this particular instance.

Elon Musk does not have $209 billion dollars, or whatever absurd dollar amount is attributed to his net worth when you happen to read this. If I own a house worth $500,000 and have $100 in my pocket, my net worth would be $500,100. But it’s misleading to say I have that much money. The vast majority of Musk’s (and all the wealthiest people for that matter) net worth is in the form of assets and specifically in this case, Tesla stock. I mentioned Tesla’s meteoric rise in valuation and it really can’t be overstated. As of writing this Tesla stock is up nearly 715% over the last year. With Musk being the top shareholder with just over 20% of shares outstanding, you can see how much his net worth is impacted by this, and we didn’t even talk about assets from his other ventures.

“But he can sell those shares just like anyone else. Stocks are fairly liquid after all.”

What would happen if Musk wanted to liquidate all his Tesla stock? Well firstly, it wouldn’t be possible in the same way it would for you or me. If he were to dump his shares on the open market, the stock price would plummet as the supply of shares immediately surpasses the demand. This isn’t even considering the panic selling that would occur when institutional and retail investors alike realize the CEO of the most valuable car company on the planet is selling his stake in the company. He could plan to sell over a long and structured period of time or conduct a block trade but this is highly illiquid and presents other problems in the context of this debate.

Musk would lose a fairly significant amount of control over Tesla due to a unique way voting is structured at the company

Musk does not have a majority stake in Tesla and each of his shares are worth one vote—same as every other shareholder—which means he technically has neither equity nor voting control. What he does have, however, is a Tesla by-law that requires a 2/3rds supermajority to make substantial changes to the company. While it’s mathematically possible to be outvoted under these circumstances, Musk’s roughly 20% stake bulwark means an improbably high consensus is needed to make a major change unsanctioned by the magnate. This is not something he is likely to give up.

But let’s pretend Musk could and would liquidate his Tesla stock today. Selling isn’t free. Perhaps the most obvious issue with this framing is that if he were to sell, he would incur taxes. Every share he sells would be subject to capital gains tax and should at least, in part, satisfy the call for wealth redistribution. A significant portion of his wealth is immediately surrendered to the government and assuming government competence, (I know, but let’s not get into that) that revenue can be put to use for the country and her people. So what we now know is that his supposed $209 billion dollars is actually mostly illiquid assets that are taxed when turned into cash.

Did we stumble upon a solution here? Though difficult, Musk could sell all his Tesla stock, and while he would not want to, maybe for the good of society he should be made to.

Would we even want him to sell?

For every seller there is a buyer and this case is no different. If Musk were to sell, the vast majority of shares would be purchased by institutional investors. The next largest shareholders after Musk are Susquehanna Securities and Capital World Investors representing 6.5% and 5.6% of outstanding shares respectively. The transfer of equity from the company’s primary innovator to large, faceless investment firms is a substantial step backward. And the more extreme alternative of a government purchase presents even more problems. Despite the increased tax revenue, a selloff is not the answer here.

So is there no solution?

The current economic system is not adequately providing financial opportunity and stability for everyone. There are many, many reasons for this and each of those reasons need to be addressed carefully as potential solutions create a host of their own problems. In order to have solutions we need to lay out the conditions of the problems coherently. We can talk about wealth redistribution, creating more competitive markets, raising or lowering taxes, and any other remedy for our economic ills. What we can’t do is describe the issues in ways that hinder our ability to understand them. We can’t misrepresent terms like “net worth” and “wealth” and perpetuate confusion. We can’t look at wealth bolstered by equity the same way we look at cash in our wallets.

You must be logged in to post a comment.